Noticeable slowdown in Dublin house price growth

Supply metrics offer some encouragement

As we head into year end, the dominant underlying feature of the Irish residential property market remains the deficit in supply. However, over the course of 2018, there has been some further improvement in the supply picture. The latest update to the CSO’s ‘new dwelling completions’ figures show that on a cumulative 12-month basis to September, the total was at 17,161 units. Comparing the first three quarters of 2018 to the same period last year shows that new supply is increasing at a rate of 28%. Extrapolating out its current pace of growth for the year as a whole, indicates that new dwellings could total around 18,500 units this year. In 2017, the full year total was 14,435.

Meanwhile, forward looking indicators, such as housing starts (as measured by commencement notices), suggest that the improving dynamic in supply continues. Commencements were up 23.5% in August on a year-to-date basis, with the 12-month running total rising to over 20,000 units. Registration figures, which are regarded as reflective of developer activity, have started to pick up again after having spent much of 2018 behind their 2017 levels. Meantime, planning permissions have surged over the past year and are up by almost 70% year-on-year in Q3. It is important that this soon translates into an acceleration in the pace of growth in house building activity.

Slower pace of price increases, lead by a marked slowdown in Dublin market.

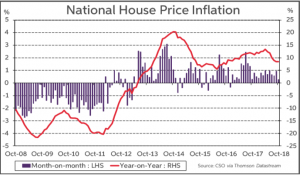

Residential property prices continue to rise at a strong pace in year-on-year terms. However, there has been a noticeable slowdown in the rate of increase since the spring. Nationally, according to the latest CSO data, house prices rose by 8.4% in October. This compares to a 13.3% yearly rate in April. The latest increase means that prices are now 84% off their low point (March 2013), but are still around 18% below their pre-crisis peak.

It is clear from the geographic breakdown, that the main origin of the slower price growth is the Dublin market. In the capital, the annual increase in prices slowed to 6.3% in October, having been as high as 13% in April. Meanwhile, non-Dublin price growth continue to outpace the Dublin market, although here too, the pace of increase has moderated, but not to the same extent. Outside the capital, prices rose by 10.6% y/y in October versus its recent high of 15.2% back in June. Analysing the Dublin market in more detail, to see where the slowdown has been most evident, offers some explanation for the slower rate of price growth. The data show that there has been a sizeable deceleration in house price inflation in most areas of the capital. This is especially evident in the more expensive ‘South Dublin’ area, where price growth has slowed to 5%. This suggests that the Central Bank mortgage rules are having an impact on house prices at the upper end of the market in Dublin.

It is clear from the geographic breakdown, that the main origin of the slower price growth is the Dublin market. In the capital, the annual increase in prices slowed to 6.3% in October, having been as high as 13% in April. Meanwhile, non-Dublin price growth continue to outpace the Dublin market, although here too, the pace of increase has moderated, but not to the same extent. Outside the capital, prices rose by 10.6% y/y in October versus its recent high of 15.2% back in June. Analysing the Dublin market in more detail, to see where the slowdown has been most evident, offers some explanation for the slower rate of price growth. The data show that there has been a sizeable deceleration in house price inflation in most areas of the capital. This is especially evident in the more expensive ‘South Dublin’ area, where price growth has slowed to 5%. This suggests that the Central Bank mortgage rules are having an impact on house prices at the upper end of the market in Dublin.

This view is supported by the recent trend of slowing activity in the mortgage market.

The BPFI statistics on mortgage approvals show that on a 12-month cumulative basis the number remains stagnant, at just below 37,000. Meanwhile, in terms of mortgage lending, growth in the volume of drawdowns slowed to 8% in the third quarter. However, the actual level of mortgage lending continues to grow strongly, albeit at a slower pace compared to last year. Mortgage lending increased by 17.5% in quarter three on a yearly basis. Taking the first three quarters, lending averaged a 21% growth rate. This compares to a 30% growth rate in 2017. The slower lending growth largely reflects the tightening of central bank mortgage lending rules in 2018.

These tighter mortgage lending rules will remain in place in 2019, suggesting that the pace of growth in house prices may moderate somewhat further next year. The relatively restrictive loan-to-income ratio of 3.5 times may also be serving as a constraint on the pace of growth in Dublin house prices. However, with the housing market remaining defined by an on-going shortfall in supply, both prices and rents are likely to continue to rise in 2019. The most critical challenge facing the sector is to ensure that the surge in planning permissions over the last year quickly translates into sharply higher levels of house building activity. There is no sign of this yet, though, in the data on new housing registrations and commencement notices. Housing output needs to double from its 2018 levels to meet annual demand and indeed, rise well above this level to meet the pent-up demand in the sector from the years of under-supply. It could be well into the next decade before supply and demand come close to balance, unless the pace of growth in house building accelerates from here.